As the world transitions to decarbonized energy systems, emerging long-duration energy storage technologies will be critical for supporting the widescale deployment of renewable energy sources.

As the world considers how to establish a path toward limiting the rise in global temperatures by curbing emissions of greenhouse gases, it is widely recognized that the power-generation sector has a central role to play. Responsible for one-third of total global carbon emissions, the sector’s role is, in fact, doubly crucial, since decarbonizing the rest of the economy vitally depends on the growing demand for renewable electricity (for example in electric vehicles and residential heating).

Most projections suggest that in order for the world’s climate goals to be attained, the power sector needs to decarbonize fully by 2040. And the good news is that the global power industry is making giant strides toward reducing emissions by switching from fossil-fuel-fired power generation to predominantly wind and solar photovoltaic (PV) power.

However, the rising share of renewables in the power mix brings with it new challenges. Not least of these are the structural strains on existing power-generation, transmission, and distribution infrastructure created by new flows of electricity and by the inherent variability of renewables, including potential imbalances in supply and demand, changes in transmission flow patterns, and the potential for greater system instability.

One answer, explored in a new industry report with insights and analysis from McKinsey, is long-duration energy storage (LDES). The report, authored by the LDES Council, a newly founded, CEO-led organization, is based on more than 10,000 cost and performance data points from council technology member companies. It argues that timely development of a long-duration energy-storage market with government support would enable the energy system to function smoothly with a large share of power coming from renewables, and would thus make a substantial contribution to decarbonizing the economy.

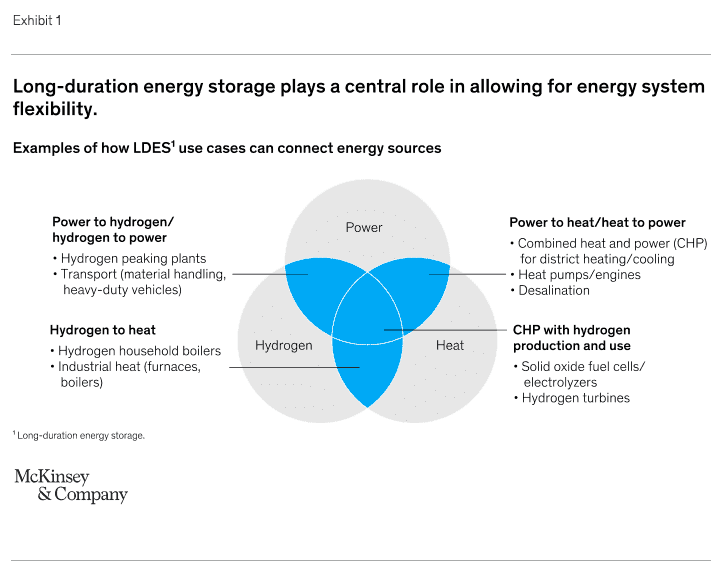

LDES encompasses a group of conventional and novel technologies, including mechanical, thermal, electrochemical, and chemical storage, that can be deployed competitively to store energy for prolonged periods and scaled up economically to sustain electricity provision, for days or even weeks. 1 What they can provide is system flexibility—the ability to absorb and manage fluctuations in demand and supply by storing energy at times of surplus and releasing it when needed. It offers a way of integrating and providing flexibility to the entire energy system, comprising power, heat, hydrogen, and other forms of energy (Exhibit 1).

The various novel LDES technologies are at different levels of maturity and market readiness, but they are attracting unprecedented interest from governments, utilities, and transmission operators, and investment in the sector is rising fast: more than five gigawatts (GW) and 65 gigawatt-hours (GWh) of LDES capacity has been announced or is already operational.

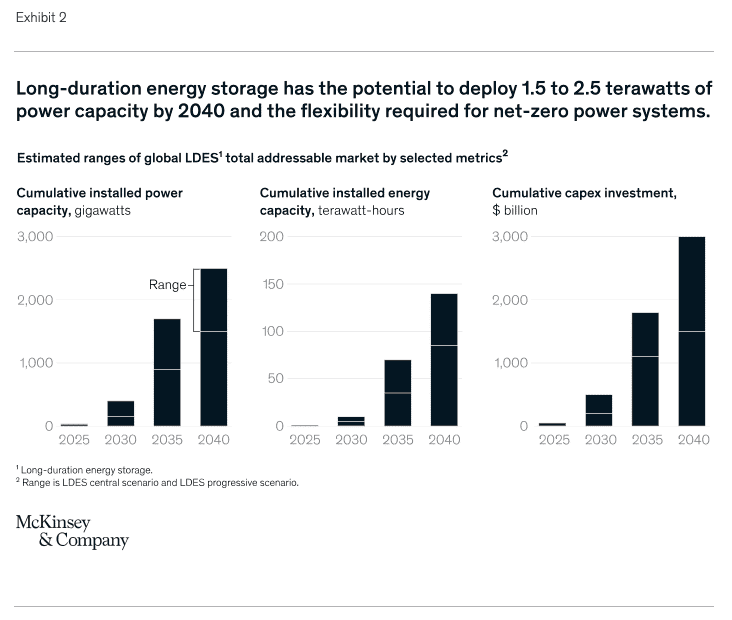

This is only a start: McKinsey modeling for the study suggests that by 2040, LDES has the potential to deploy 1.5 to 2.5 terawatts (TW) of power capacity—or eight to 15 times the total energy-storage capacity deployed today—globally. Likewise, it could deploy 85 to 140 terawatt-hours (TWh) of energy capacity by 2040 and store up to 10 percent of all electricity consumed. This corresponds to a cumulative investment of $1.5 trillion to $3 trillion (Exhibit 2).

We estimate that by 2040, LDES deployment could result in the avoidance of 1.5 to 2.3 gigatons of CO2 equivalent per year, or around 10 to 15 percent of today’s power sector emissions. In the United States alone, LDES could reduce the overall cost of achieving a fully decarbonized power system by around $35 billion annually by 2040.

The scale of these numbers reflects the multiple use cases for LDES technologies and the central role they can play in balancing the power system and making it more efficient. These include support for system stability, firming corporate power-purchase agreements, and optimization of energy for industries with remote or unreliable grids. But by far the largest proportion of deployment is expected to be related to the central tasks of energy shifting, capacity provision, and transmission and distribution (T&D) optimization in bulk power systems (see Exhibit 2).

One key benefit of LDES is that it entails low marginal costs for storing electricity: it enables the decoupling of the quantity of electricity stored and the speed with which it is taken in (charged) or released (discharged); it is widely deployable and scalable; and it has relatively low lead times when compared with the upgrading of T&D grids. This makes it competitive with other forms of energy storage such as lithium-ion batteries, dispatchable-hydrogen assets, and pumped-storage hydropower, and economically preferable to expensive and protracted grid upgrades. Indeed, the evidence shows that in many applications, it is likely to be the most cost-competitive solution for energy storage beyond a duration of six to eight hours.

As a result, while novel LDES technologies are still nascent, deployment could accelerate rapidly in the next few years. Our modeling projects installation of 30 to 40 GW power capacity and one TWh energy capacity by 2025 under a fast decarbonization scenario.

A key milestone for LDES is reached when renewable energy (RE) reaches 60 to 70 percent market share in bulk power systems, which many countries with high climate ambitions aim to reach between 2025 and 2035. This would likely include the United Kingdom, the United States, and many other developed countries which have made net-zero commitments prior to the COP26 Climate Change Conference in Glasgow in November. This RE penetration catalyzes widespread deployment of LDES as the lowest-cost flexibility solution.

Hitting these targets requires significant reductions in the cost of LDES technologies. But projections provided by LDES Council member companies show these are achievable and in line with learning curves experienced in other nascent energy technologies in the recent past, including solar PV and wind power. In turn, cost reductions will be dependent on improvements in R&D, volumes deployed, and scale efficiencies in manufacturing. Similarly, total LDES deployment is closely tied to the rate of decarbonization of the power sector and the deployment of variable RE generation.

All this means that in the short to medium term, government action will be required to kick-start an LDES market by lowering costs, mobilizing the necessary investment capital, and creating a market ecosystem enabling investors to make an attractive return on LDES. Policy makers can help in three ways:

- Long-term system planning, including clear targets for renewables’ share in the power-generation mix and the infrastructure required to maintain system stability, is critical to underpinning investor confidence. Examples of this are already under way in California and New South Wales among other places.

- Government support for early deployments of LDES would help derisk the market for investors and enable the market to scale. Dedicated support programs for large-scale demonstration plants would ensure that these technologies can reach their full technological and cost-reduction potential and that new market mechanisms can be tested. Examples include the United Kingdom, where the government launched a $100 million LDES demonstration competition in early 2021 to accelerate project commercialization, and the United States, where the Department of Energy is overseeing a $1 billion program (“Earthshot’’) to reduce the costs of LDES systems with more than ten hours of storage capacity by 90 percent in ten years.

- Creation of supportive market designs, such as capacity mechanisms and policies that capture the full value of LDES, would enable investors to receive investable returns with acceptable risk. At present, this is not possible since power markets are mostly short term; multiday and multiweek market signals are weak compared to intraday; and carbon-reduction compensation schemes either do not exist or are insufficient to compensate investors for the additional funding. But some frontrunners—including California and Arizona—have produced examples of legislation explicitly designed to meet the needs of LDES. Arizona has launched an incentive program structured to encourage longer durations by offering incentives for storage technologies with more than five hours of discharge.

Together, these measures will ultimately help ensure that the energy transition is achieved at the lowest societal cost. The projections in the study show that with early deployments and a supportive market ecosystem, LDES applications can achieve internal rates of return (IRRs) well above investor hurdle rates by 2025—comparable with benchmarked IRRs of current mature energy projects.

The benefits to society of large-scale LDES deployment as solar PV and wind become the dominant sources of power are obvious: the alternatives are costlier; and failing to invest in system flexibility as the renewable share of the power mix grows would be a recipe for major instability in electricity supply.

Furthermore, all the evidence suggests that this could be a highly attractive market for investors: a sizeable new industry providing 1.5 to 2.5 TW of storage capacity, requiring an investment that could reach $1 trillion to $3 trillion by 2040 with potential competitive returns. The prize is within reach, and the time to seize it is now.

Source : McKinsey.com